Why it matters when buying land

Floodplain land is frequently the cheapest land on the market, and for a reason: building in it is restricted, expensive, or sometimes effectively prohibited. Local floodplain ordinances typically require elevated construction, special permits, and engineering — and the floodway (the channel that must stay clear to carry flood water) is usually off-limits to structures entirely.

Even where building is allowed, flood risk affects everything downstream of the purchase: insurance costs, financing, resale value, and the practical usability of the land during wet seasons.

Floodplains are not worthless, though. They can be excellent for pasture, recreation, timber, and wildlife habitat — the key is buying them at floodplain prices with accurate expectations, not discovering the designation after closing.

How to check it

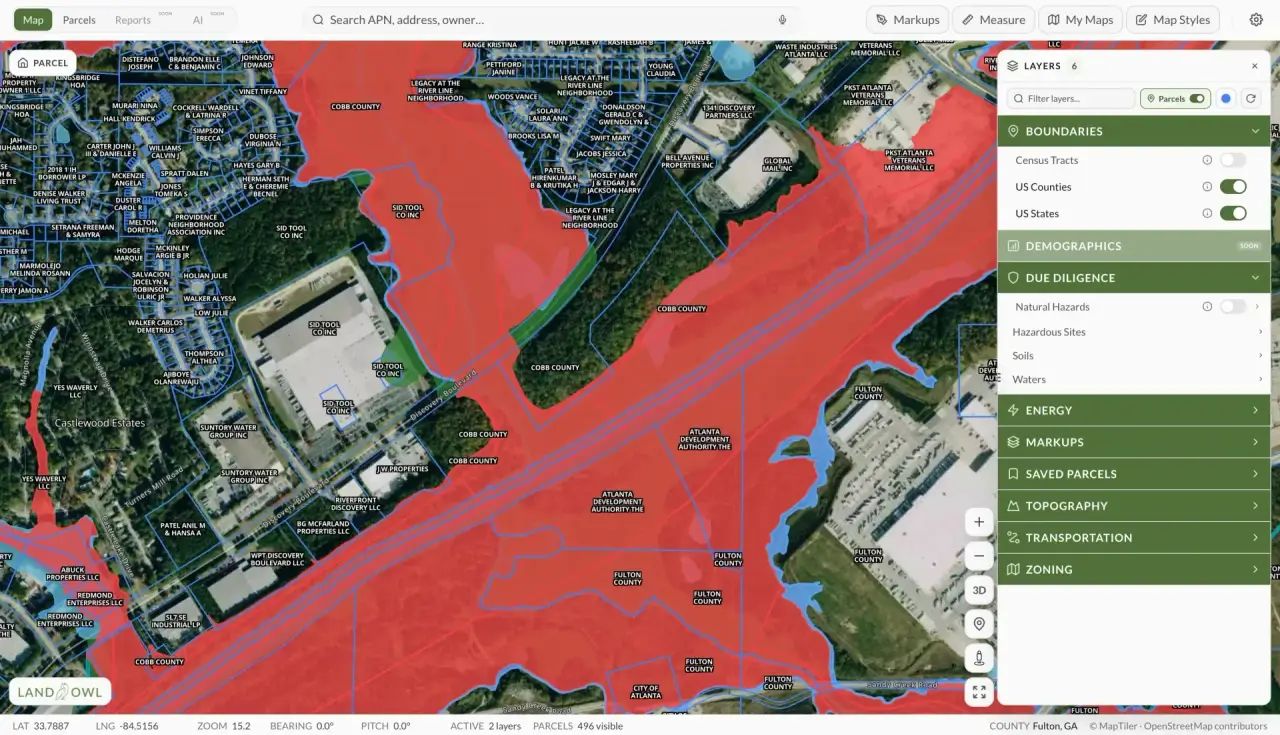

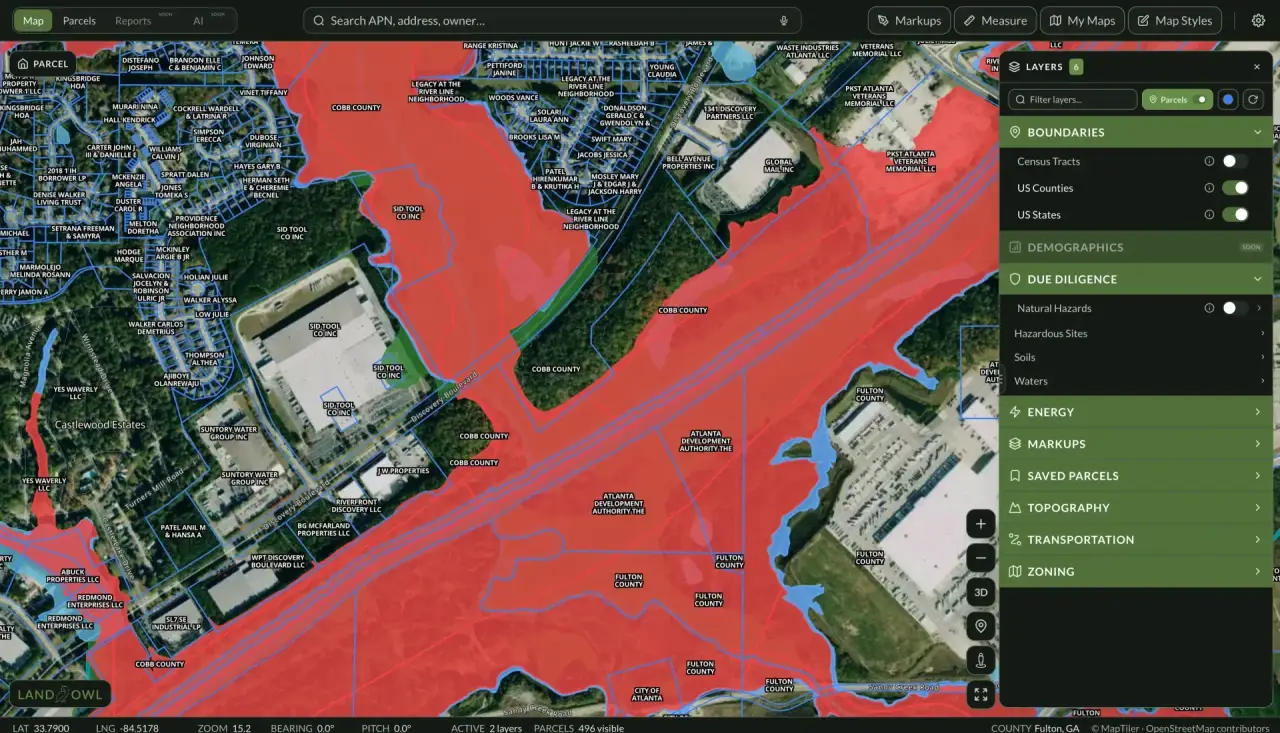

Check the parcel against FEMA's flood maps — in Land Owl, the FEMA flood zone layer shows the mapped floodplain boundaries directly over the parcel lines, so you can see how much of the parcel is affected and whether any upland building area remains.

Look at the land itself and its surroundings: proximity to streams and rivers, low elevation relative to nearby water, flat bottomland terrain, and water-tolerant vegetation are all physical floodplain indicators. County GIS sites often layer flood data with topography.

Ask the local floodplain administrator (most communities in the National Flood Insurance Program have one) what the parcel's designation means for permits, and ask neighbors or the county about actual flooding history — real events sometimes exceed what the maps show.

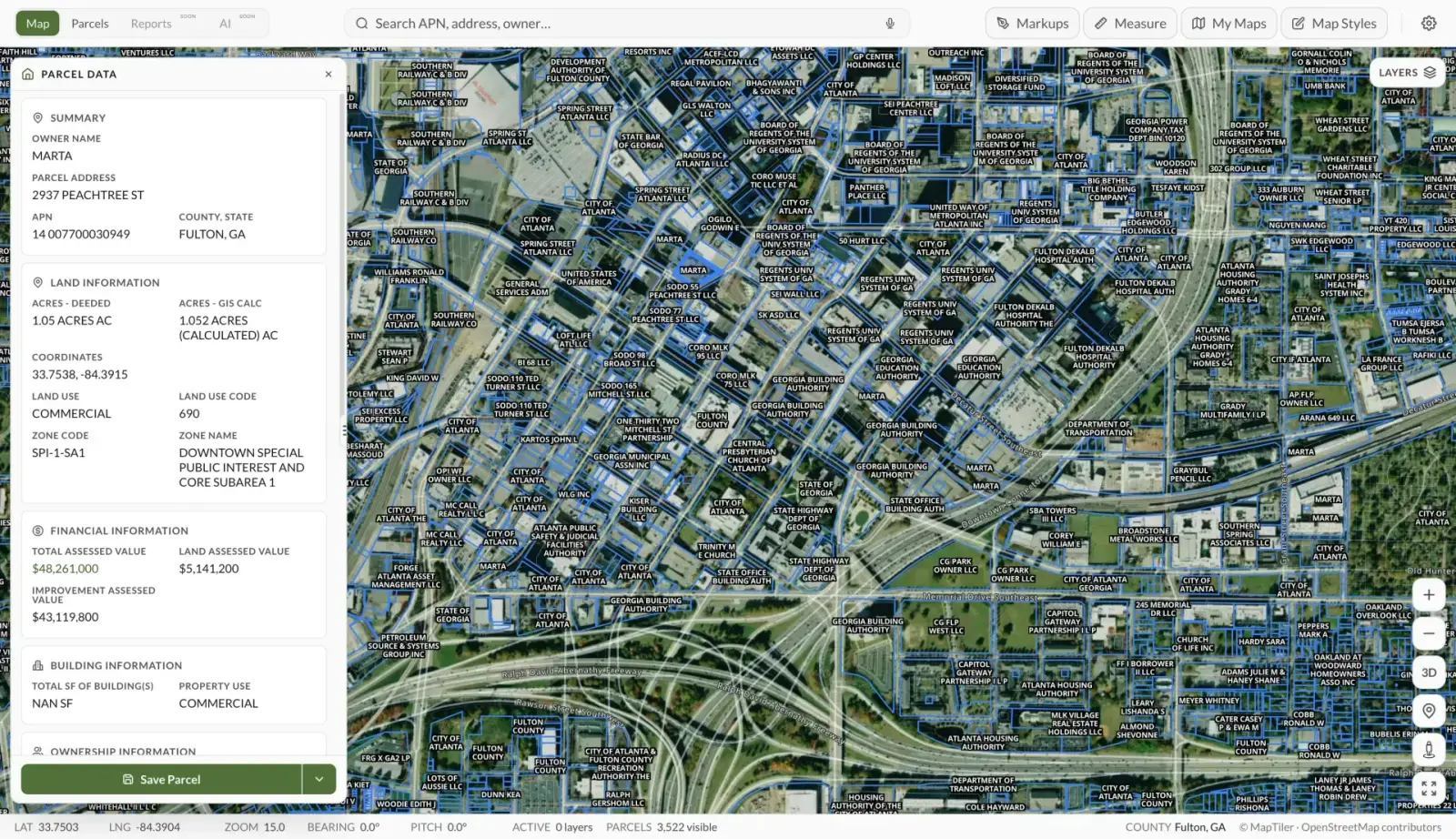

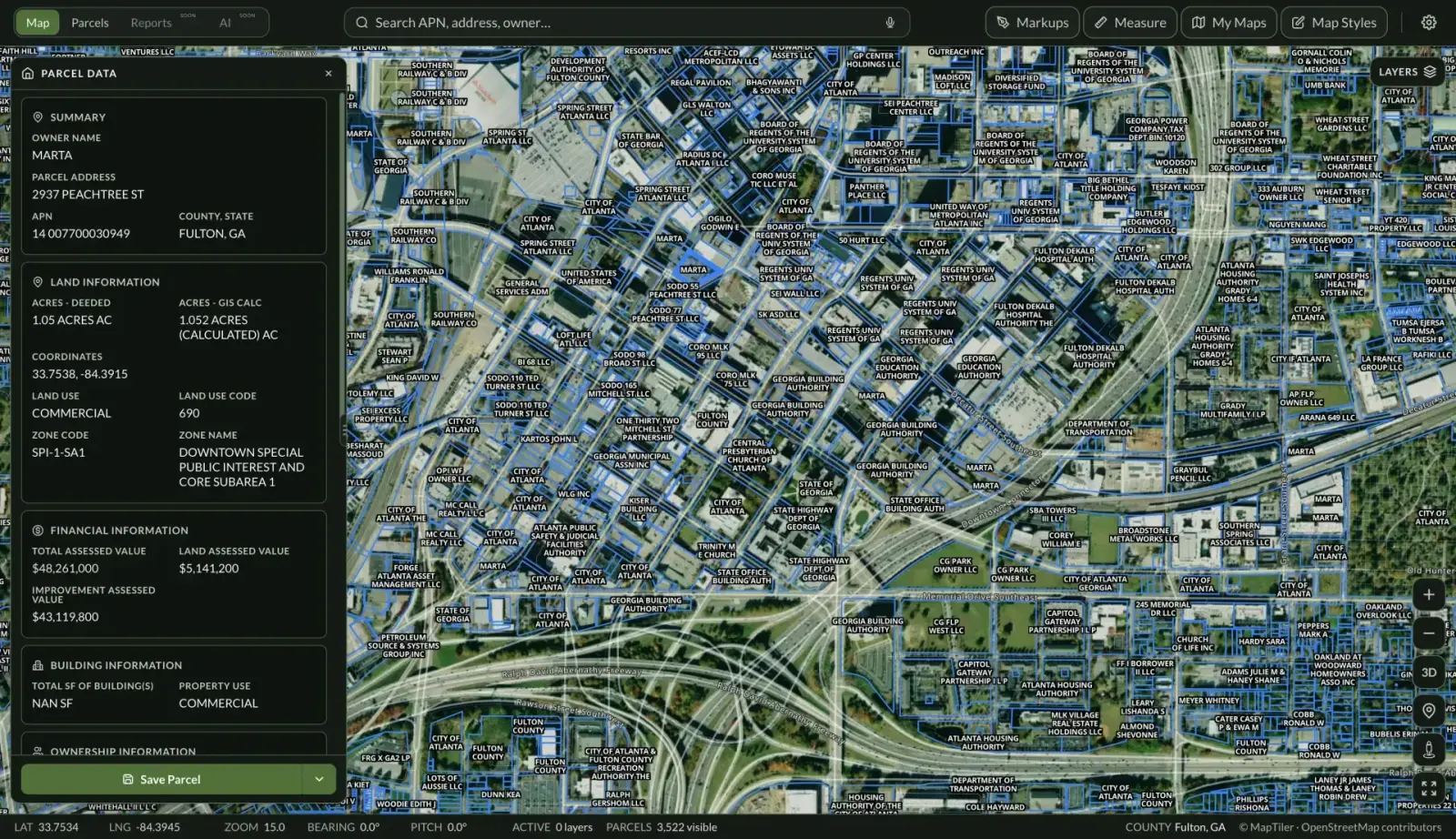

See it on a real parcel

Land Owl overlays zoning, ownership, flood risk, and more on every parcel — before you commit a dollar.

What is the difference between a floodplain and a flood zone?

A floodplain is the physical landform — the low ground that water spreads onto during a flood. A flood zone is FEMA's regulatory classification of that risk on a Flood Insurance Rate Map, such as Zone A, AE, VE, or X.

The two usually overlap but are not identical: maps lag reality, and land can flood without being in a mapped high-risk zone. Treat the FEMA zone as the regulatory answer and the terrain and flood history as the practical one.

What is the difference between the floodway and the flood fringe?

Regulators split the 1%-annual-chance floodplain into two parts. The floodway is the stream channel plus the adjacent land that must remain open to convey flood water — new structures and fill are generally prohibited there because they would push flood levels higher onto other properties.

The flood fringe is the rest of the floodplain, where development is usually allowed subject to conditions like elevating the structure above the base flood elevation. Exact rules come from the local floodplain ordinance and vary by community.

Can you build on land in a floodplain?

Often yes, in the flood fringe — but under conditions. Typical requirements include a floodplain development permit, elevating the lowest floor at or above the base flood elevation (some communities require extra “freeboard”), flood-resistant materials, and engineered foundations.

In the floodway, building is generally prohibited or requires an engineering study proving no rise in flood levels. All of this adds cost, so a floodplain parcel needs a price that reflects it. Requirements vary by county and state, so confirm specifics with the local floodplain administrator before buying.

Is floodplain land a bad investment?

Not inherently — it depends on the intended use and the price. Floodplain acreage can be productive farmland, pasture, timberland, or hunting and recreation land, and parcels that are partly floodplain often have perfectly buildable upland portions.

The bad outcomes come from mismatched expectations: paying buildable-lot prices for land that cannot support a house, or underestimating insurance and construction costs. Map the floodplain boundary against your actual plans before making an offer.